Take an ice cube out of the freezer on a hot afternoon and put it on a plate.

For the first few minutes, it barely sweats.

Half an hour later, there's a small puddle.

By the final stretch of sunlight, it's melting so fast you can watch it shrink.

Nothing attacked the ice cube.

Nothing touched it.

Time did that.

An option's premium is an ice cube.

Part of what you pay for any option is time value — the market's price for "something could still happen before this contract ends."

And time value has one non-negotiable property: it melts. Every hour. Every day. Faster and faster as expiry approaches.

Traders call this melt theta. You can just remember the ice cube.

On expiry day itself, the melt hits maximum speed.

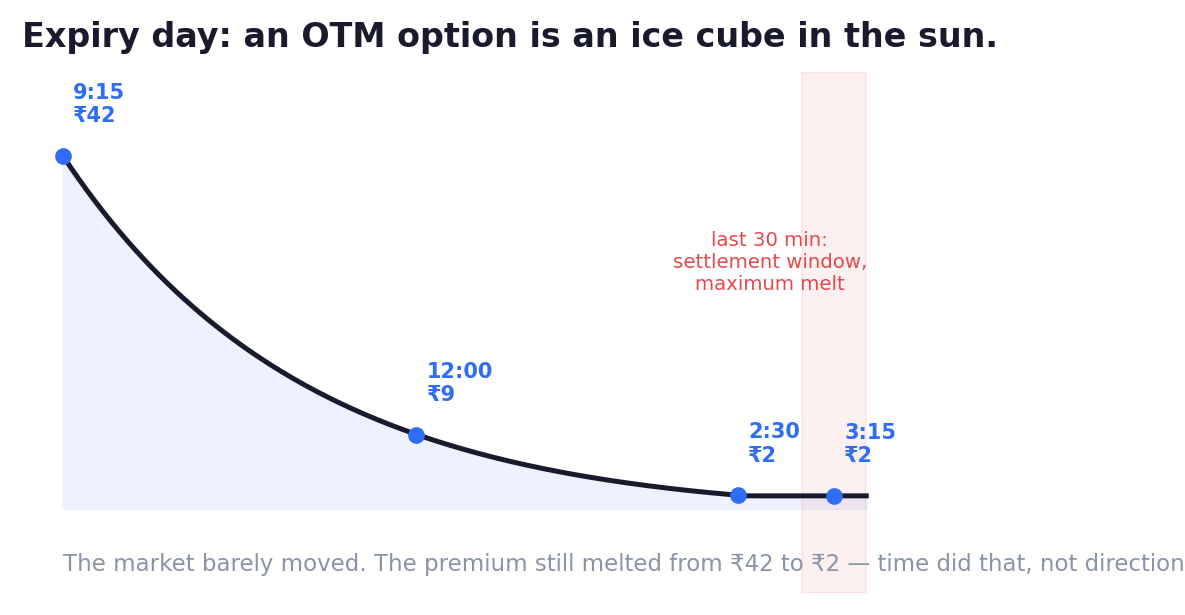

An out-of-the-money option can open at ₹40 in the morning and be worth ₹2 by 3:15 — even if the market barely moves.

Read that again, because it breaks most beginners' mental model of options:

On expiry day, you can be right about the market and still lose — because the melt outran the move.

Quick India context, because expiry here has its own rhythm.

Since September 2025, Nifty weekly options expire every Tuesday on NSE, and Sensex weekly options every Thursday on BSE. Monthly contracts follow the same days — the last Tuesday and last Thursday of the month. (If expiry falls on a holiday, it shifts to the previous trading day.)

Which means the Indian market effectively has an "expiry personality" twice a week.

And that personality is strange. Here's what expiry does to price itself:

- Enormous option positions are being closed, rolled and unwound all day, so price action turns noisy and mechanical rather than story-driven.

- Price often turns sticky around big round strikes — the levels where the largest number of contracts sit. Traders describe it as pinning, like the strike is a magnet. (You may also hear the phrase max pain — the level at which the largest number of option buyers finish worthless.)

- The final thirty minutes — the 3:00 to 3:30 window whose average decides the final settlement price — can whip violently in both directions as the last positions square off.

So what's the playbook?

Here's the honest answer, and it may not be the one you wanted.

For most traders, the expiry-day playbook is defence, not attack.

- That ₹5 option that looks like a cheap lottery ticket? It's priced by people who understand the melting. Buying cheap options on an expiry afternoon "because they're only ₹5" isn't a play. Over time, it's a donation — with occasional jackpots designed to keep you donating.

- If you do trade expiry: smaller size than usual, defined risk, and full awareness that the ice is melting under you every single minute you hold. On expiry day, time charges rent by the hour.

- The traders who consistently earn from the melt are option sellers — but selling options carries serious risks and margin requirements of its own, and belongs in a later, more advanced school. Knowing the melt exists does not mean you're ready to harvest it.

Plenty of consistently profitable traders have a one-line expiry playbook:

"I don't."

That is a real playbook.

It goes in the menu like any other.

Key Takeaway

On expiry day, time is a bigger force than direction. Premiums melt fastest in the final hours, price gets magnetic near crowded strikes, and 'cheap' options are priced by people who understand the melting. Defence first.

Think About It

If an option can lose ninety percent of its value on a day the market goes nowhere — what exactly were you buying, the last time you bought a ₹5 option at 1 p.m. on a Tuesday?

Playbook Lab — Watch the Ice Melt

Next Tuesday, run this experiment with zero money:

Pick one out-of-the-money Nifty option at 9:15 and write down its price.

Check it again at 12:00, at 2:30, and at 3:15 — each time noting where Nifty itself is trading.

Watch what "the market did nothing" does to that premium.

One observed melt teaches more than any definition of theta ever will.