THE THEORIST

Who

George Soros (b. 1930), Hungarian-American investor and philosopher-manqué

When & where

New York; the theory formalised in 1987 after decades of running the Quantum Fund — with roots in his student years under philosopher Karl Popper in London

Why he built it

Soros survived Nazi-occupied Budapest as a boy, then studied philosophy — and noticed markets violated the assumption behind all equilibrium economics: the observer changes the observed. He traded that insight for decades before writing it down

The work

'The Alchemy of Finance' (1987); restated in lectures and essays for thirty years since

The demonstration

1992: his fund's bet against the British pound — a currency defence collapsing under the weight of speculation ABOUT its collapse — made ~$1 billion in a day and made reflexivity impossible to ignore

Portrait sourcing

Wikimedia Commons: 'George Soros' (CC-licensed, many)

Every theory so far shares one hidden assumption. Time to break it.

The assumption: prices are mirrors. Out there is reality — companies, profits, economies — and the market's job is to reflect it. Efficient markets said the mirror is fast and accurate. Behavioural finance said the mirror is wobbly and emotional. But both agreed on the direction: reality on one side, reflection on the other.

George Soros made his fortune on a heresy: the mirror changes your face.

The man matters here, because the theory grew from a life. Soros survived Nazi-occupied Budapest as a Jewish teenager — a year, he later said, that taught him how quickly 'reality' can be remade by collective belief. He studied philosophy in London under Karl Popper, obsessed with a problem most economists ignored: in human systems, the observer participates in what he observes. Then he went into markets, ran one of the most successful funds in history, and in 1987 finally wrote down the idea he claimed to be trading all along. He called it reflexivity.

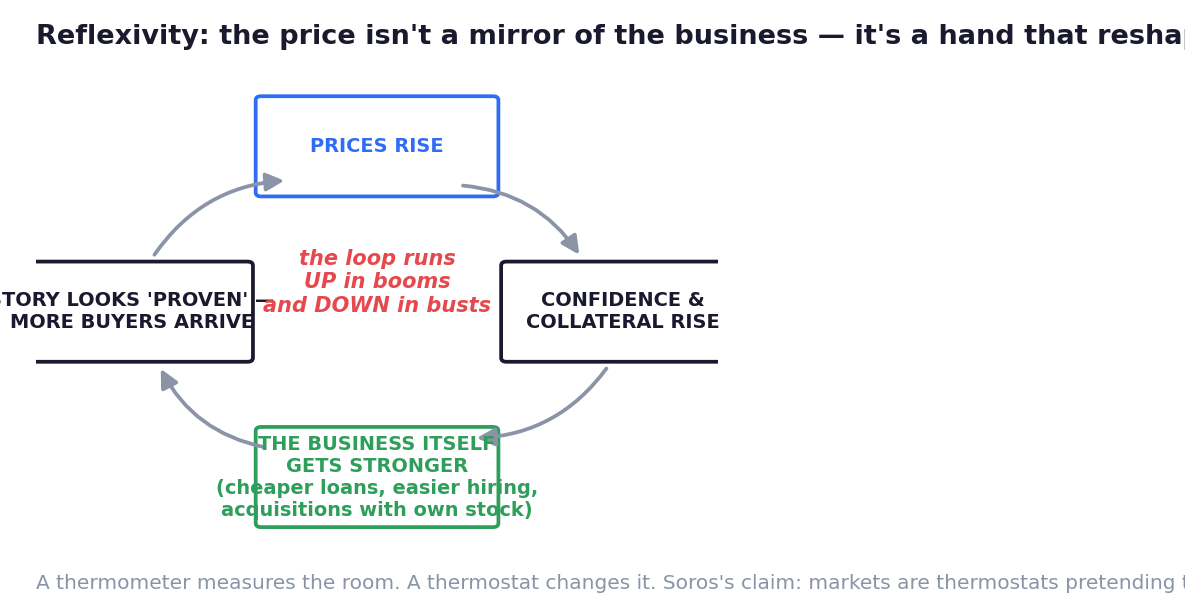

Here's the theory, stripped to its engine — and the figure shows the loop:

In markets, causation runs in both directions at once:

Reality shapes prices — everyone accepts this. Good company, rising price.

But prices also shape reality. A rising stock price is not just a reflection — it's a tool the company can use: cheaper loans (its collateral is worth more), easier hiring (stock compensation attracts talent), acquisitions paid for with its own inflated shares, customers and partners who trust it more because the market seems to. The rising price improves the fundamentals — which justifies a higher price — which improves them further...

A thermometer measures the room. A thermostat changes it. Soros's claim: market prices are thermostats wearing thermometer costumes.

Once you see the loop, the market's most puzzling behaviours stop being puzzling:

Why do bubbles last so long? Because for years, a bubble is not a lie. The loop genuinely delivers: the loans really are cheaper, the acquisitions really happen, the profits really grow. Analysts pointing at 'improving fundamentals' aren't hallucinating — they're watching the price manufacture fundamentals. The boom validates itself... until the gap between the story and what the loop can actually sustain grows too wide.

Why are busts so violent? Because the loop has a reverse gear, and it's crueller: falling prices destroy collateral, trigger margin calls, frighten lenders, repel customers — worsening the fundamentals, justifying lower prices. The same machine that built the boom dismantles it, faster. (Walk through the School of Market History and you'll see this loop in nearly every exhibit: 1929's margin spiral, 2008's collateral collapse.)

And why did a currency fall to bets about its falling? In 1992, Soros's fund famously bet billions against the British pound, which was pegged at an unsustainable level. The bet itself — and the wave of speculation it emboldened — created the pressure that broke the peg. The prophecy caused its own fulfilment: reflexivity, demonstrated for roughly a billion dollars of profit in a single day, at a scale nobody could dismiss.

Where the lens breaks — honestly:

Reflexivity is a brilliant description and a frustrating predictor. It tells you loops exist; it doesn't tell you when they flip. Soros himself lost money being early. Academics long grumbled that it's more philosophy than testable theory (though 'self-fulfilling' dynamics are now studied seriously across economics). Treat it as Chapter 1 taught: a hand on a real part of the elephant — the alive part — not the whole animal.

How to actually use it — three habits:

Ask the loop question about any strong trend: is this price merely reflecting the business — or feeding it? Does the company raise money, borrow, hire or acquire using its own price? The more yes, the more reflexive — the further it can run past 'rational', and the harder it will unwind.

Respect booms you disbelieve. A reflexive boom is temporarily self-justifying — being 'right' about the overvaluation is not enough (the Market History school priced that lesson in a chapter about a squeezed stock). Position size, not outrage.

And in busts, remember fundamentals are falling WITH the price, not standing still beneath it. 'It's cheap because nothing changed' misreads a reverse loop, where the falling price is itself changing everything.

The mirror moves when you look at it.

Trade accordingly.

Key Takeaway

Soros's heresy: prices don't just reflect reality — they reshape it. Rising prices manufacture better fundamentals (cheaper capital, easier hiring, richer acquisitions) and falling prices destroy them, which is why bubbles self-justify for years and busts overshoot. Ask of every strong trend: is the price feeding the business it claims to measure? Size positions for loops, and never argue with one on schedule.

Think About It

Pick the strongest trend in today's markets — any country, any asset. Is its price merely reflecting its story... or actively funding it? What specifically breaks first if the price stops rising?

Theory Lab — Map a Loop

Choose one famous boom — current or historical (a tech giant, a housing market, a crypto cycle).

Draw its loop on paper, four boxes like the figure: price rises → what improves BECAUSE of the price? (loans, hiring, acquisitions, trust) → how does that improvement justify a higher price? → repeat.

Then draw the reverse gear: if the price fell 40%, what breaks first? What does that breakage do to the price?

Finish with one line: "This trend is __% mirror, __% thermostat." There's no exact answer — the estimate itself is the skill, and almost nobody around you is even asking the question.