THE THEORIST

Who

Harry Markowitz (1927–2023), American economist

When & where

University of Chicago, 1952 — he was a 25-year-old PhD student

Why he built it

Reading about stock valuation in a library, he noticed the theory said 'pick the best stock' — but real investors obviously cared about the RISK of the whole collection. Nobody had mathematised that. So he did, before finishing his degree

The work

'Portfolio Selection', Journal of Finance, 1952 — about fourteen pages

Recognition

Nobel Prize 1990. At his thesis defence, the legendary Milton Friedman reportedly objected that the work 'wasn't even economics'. Revolutions rarely look like the old subject

Portrait sourcing

Wikimedia Commons: 'Harry Markowitz' (CC-licensed, Nobel-era)

Every culture on Earth has the proverb. Eggs. Baskets. Don't.

For thousands of years it stayed folk wisdom — obviously sensible, never examined. Then in 1952, a 25-year-old graduate student named Harry Markowitz, sitting in a Chicago library, asked the childishly simple question nobody had mathematised:

If I hold several investments... what is the risk of the whole basket?

His fourteen-page answer earned a Nobel Prize and quietly redesigned how the world's money is managed. Because the answer was not what anyone assumed:

The risk of a basket is NOT the average risk of the things inside it.

It depends — decisively — on a word investors had barely used before 1952: correlation. Do the things in your basket move together, or differently?

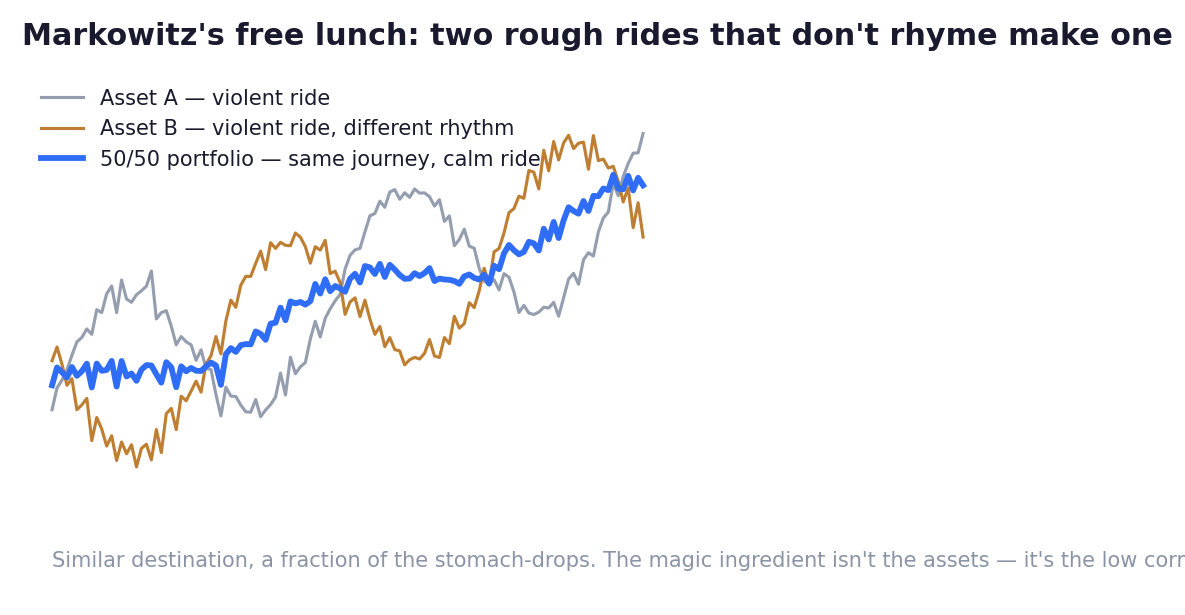

Feel it with the figure. Two investments, both violently bumpy, both ending in the same good place — but bumping at different times: when one lurches down, the other happens to be lurching up.

Hold either alone: a stomach-churning ride.

Hold half of each: the lurches partially cancel. Same destination. Dramatically smoother road.

And here's what made economists fall out of their chairs: nothing was sacrificed. No return given up. The smoothness appeared out of pure mathematics — out of the relationship between the assets rather than the assets themselves. In a field where every reward demands a matching risk, this was the exception — which is why diversification earned the most famous nickname in finance:

The only free lunch in investing.

But (and this 'but' is where most portfolios quietly fail) the lunch has one condition, and it's the entire skill:

Diversification is about correlation, not count. Thirty stocks that all rise and fall with the same market mood are one bet wearing thirty costumes. Meanwhile two assets that answer genuinely different questions — stocks (growth), government bonds (stability), gold (chaos insurance), assets from other economies — can diversify better than thirty lookalikes. Count your bets, never your holdings.

Two footnotes from Markowitz's own life, both worth more than they seem:

At his thesis defence, the great economist Milton Friedman reportedly grumbled that the work wasn't mathematics, wasn't economics, wasn't even business administration. Markowitz got the PhD anyway — and, in 1990, the Nobel. (File under Chapter 1: new hands on the elephant always look wrong to the old hands.)

And when asked how he invested his own retirement savings, the father of portfolio mathematics confessed he simply split them half-and-half between stocks and bonds — to minimise his future regret. Read that twice. The man who turned risk into equations chose his own portfolio to protect his feelings. Even the mathematician respected the animal who'd have to live with the outcome — a truth Chapter 6 measures precisely.

One honest warning before the lab, written in the blood of 2008:

In a true panic, correlations rise toward one. When everyone must sell everything to raise cash, 'different' assets fall together — thirty stocks, forty stocks, it doesn't matter; the market becomes one trade. The free lunch survives crashes only across genuinely different asset classes and geographies — plus plain cash, the one thing that never joins the panic. Diversification is superb weather protection. For earthquakes, you need supplies from a different tectonic plate.

How to use the lens — three moves, applicable in any country:

Judge additions by the basket. 'Is this a great stock?' is an incomplete question. 'What does adding it do to my basket's behaviour?' is the complete one. Something mediocre alone can be brilliant in combination — that was the whole revolution.

Spread across questions, not tickers. Own things that answer different futures: growth assets, stability assets, chaos insurance, other economies. Your home market — whichever it is — is one bet, however many stocks you own inside it.

Rebalance on a calendar. Once or twice a year, trim what grew and top up what lagged, back to your target mix. It's unglamorous — and it's the machine that actually harvests the free lunch, forcing you to sell euphoria and buy gloom without needing courage in the moment.

Grandmother, it turns out, was doing mathematics all along.

She just never wrote the fourteen pages.

Key Takeaway

Markowitz proved risk lives in how holdings move together, not in holdings alone — making low correlation the only free lunch in investing. Eat it correctly: judge every addition by what it does to the basket, count bets instead of tickers, spread across asset classes and geographies, rebalance on a calendar — and remember panics push correlations toward one, so keep supplies on another tectonic plate.

Think About It

In the last sharp market fall you experienced, how many of your holdings went down together, on the same days, for the same reason? Were you diversified — or fragmented?

Theory Lab — Count Your Bets

List everything you own — stocks, funds, property, gold, cash, crypto, whatever applies.

Now regroup the list ruthlessly by what actually DRIVES each item: 'my home country's stock market mood' is one group, however many holdings sit in it. 'Interest rates.' 'One employer' (salary counts!). 'One property market.'

Count the groups. That number — not your holdings count — is your true diversification.

Finish the sentence in writing: "My portfolio is really ___ bets, dressed as ___ holdings."

If the first number is 1 or 2, you've found this chapter's homework — and put a rebalancing date in your calendar before closing this page.