THE THEORIST

Who

Everyone and no one — a folk theory, older than stock markets, practised in every mania since tulips

The formal cousin

John Maynard Keynes (1883–1946) — the century's most famous economist, and a superb investor — who described the mechanism precisely in 1936

When & where

'The General Theory', Chapter 12 (1936) — his 'beauty contest' passage, written after living through (and trading through) the 1929 mania

The insight

Professional speculation is often not about picking the best asset — it's about picking what OTHERS will think others will pick: anticipating average opinion about average opinion

The rule of the game

Any price is 'rational' to pay if a greater fool follows. The theory's entire content is one question: what if you're the last one?

Portrait sourcing

Keynes: public domain / Wikimedia Commons 'John Maynard Keynes'

Every theory so far tried to answer what things are worth. This one, with magnificent honesty, doesn't care.

The Greater Fool Theory says: the worth doesn't matter. Only the queue matters.

You can knowingly, cheerfully overpay for anything — a stock at absurd multiples, a digital picture of a rock, a house, a tulip bulb — and still profit handsomely, provided one condition holds: a greater fool arrives after you, willing to pay more. Your purchase isn't a valuation. It's a bet on the existence of your successor.

Nobody 'invented' this theory. It's folk wisdom, older than exchanges, rediscovered by every generation in every mania — which is exactly why it belongs in this school: it's the theory people trade while claiming to believe the others.

But its finest formal description comes from a giant: John Maynard Keynes — the most famous economist of the twentieth century and, unusually for a theorist, a genuinely successful investor who had traded through the 1929 madness. In 1936 he explained professional speculation with a newspaper game of his era:

Papers would print a hundred photographs and award a prize to the reader who picked the faces most picked by other readers. The naive player chooses the faces he finds prettiest. The smarter player chooses the faces he thinks others will find prettiest. The professional, Keynes observed, plays a level higher still: choosing what average opinion expects average opinion to be — beauty itself having quietly left the game entirely.

That's the greater-fool machine in formal dress: at some point in every mania, participants stop asking "what is this worth?" and start asking "what will the next person pay?" — and the market becomes a beauty contest about a beauty contest, floating free of the asset underneath.

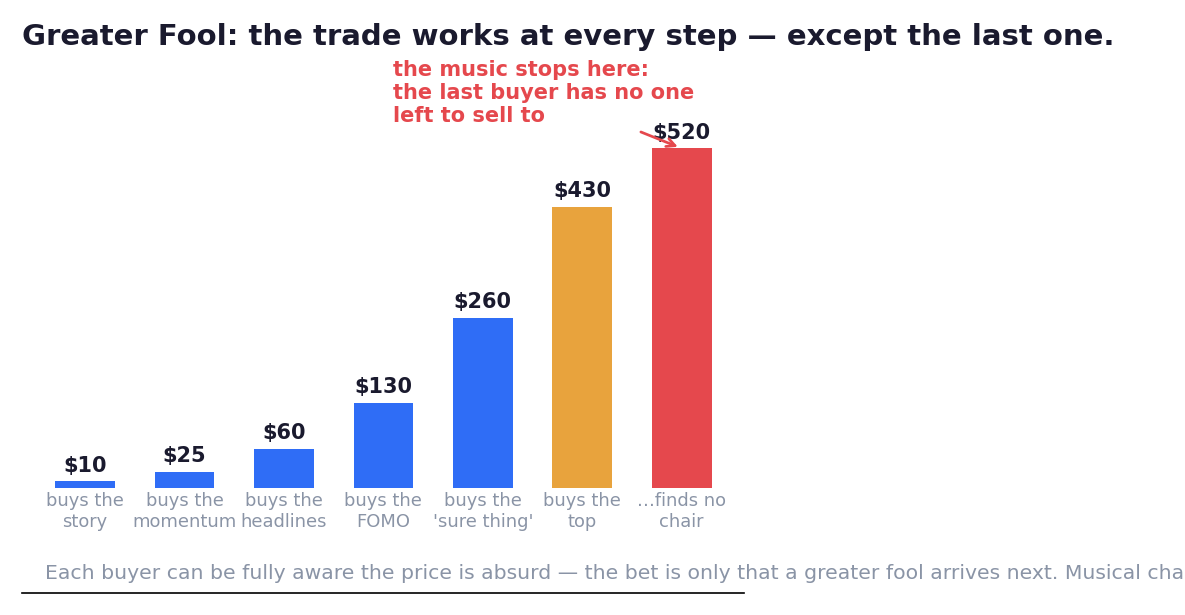

Now look at the figure — the game as a bar chart — and notice the theory's three uncomfortable truths:

Truth one: the fools aren't foolish — until one is. Every buyer in the chain except the last one made money. The early buyers of history's silliest bubbles did spectacularly well. Greater-fool buying isn't irrational at each step; it's a rational bet on the queue continuing. That's what makes it so seductive — and so dangerous: the strategy works right up until the moment it catastrophically doesn't, and nothing about your own purchase tells you which buyer you are.

Truth two: the music always stops, and always for the same reason. A mania needs a growing supply of new buyers — and humans are finite. When everyone who could be persuaded has bought (your colleagues, your barber, the news anchors), the queue simply... ends. No villain required, no headline needed. The last fool isn't dumber than the others. He's just later — holding the parcel when the room ran out of hands. (And Chapter 6 explains why he then can't sell: realising the loss hurts twice as much as hoping.)

Truth three: you cannot sit out by being right. Knowing a price is absurd tells you nothing about timing — reflexive loops (Chapter 7) can feed a queue for years, and betting against a mania early has bankrupted brilliant people (the Market History school keeps their portraits). The theory's practical demand isn't superiority. It's self-location.

So here is the entire practical content of this ancient theory, one question long:

*"If I buy this — which buyer in the chain am I?"*

Buying a sound asset for its own worth, indifferent to the queue? You're not playing this game at all — carry on. Buying early into momentum with defined risk, knowing exactly what game it is? A legitimate professional trade — musical chairs played with an exit plan and a hand hovering near a chair. But buying because it's already up 400%, because everyone's talking about it, because you can't stand watching others get rich — with no exit rule and full size?

Then the honest answer to the question is the one nobody gives in time:

The queue is what you were recruited for.

The music is lovely, though. It always is, near the end.

Key Takeaway

The greater fool game: any price is fine if a later fool pays more — Keynes formalised it as a beauty contest about a beauty contest, where worth leaves the room. Early fools profit, the last fool merely arrived late, and being 'right' about absurdity is worthless without timing. The theory's whole use is one question, asked before every hot purchase: which buyer in the chain am I — and where, exactly, is my chair?

Think About It

The most exciting asset in your world right now — the one everyone's discussing: if you bought it today, complete honestly: 'I am buyer number ___ in the chain, and my plan when the music stops is ___.' If the second blank is empty, you have your answer.

Theory Lab — The Chair Check

Pick the hottest asset currently in your feeds — stock, coin, sector, anything.

Answer four questions in writing:

You may still buy — the theory doesn't forbid the game; it forbids playing it unknowingly. The lab's product is one sentence, kept where you can see it: 'If I'm in a queue, I know it, and I know my chair.'