THE THEORIST

Who

Eugene Fama (b. 1939), American economist, University of Chicago — with deep roots in Louis Bachelier (1870–1946), a French mathematician ignored for 60 years

When & where

Chicago, 1965 (PhD thesis) and 1970 (the famous framework paper) — the age of computers first crunching decades of price data

Why he built it

Fama started college helping a professor find market-beating trading rules. The rules kept working on past data and failing on new data. He asked why — and the answer became EMH

The work

'The Behavior of Stock Market Prices' (1965); 'Efficient Capital Markets' (1970)

Recognition

Nobel Prize 2013 — shared, beautifully, with Robert Shiller, who spent his career documenting where efficiency FAILS

Portrait sourcing

Wikimedia Commons: 'Eugene Fama' (CC-licensed, Nobel-era photos); Bachelier portrait is public domain

Start with the joke, because the joke is the theory.

Two economists walk down a street. The younger one stops: "Look — a $100 bill on the sidewalk!"

The older one doesn't even look down. "Impossible. If it were real, someone would have picked it up already."

Everyone laughs at the old economist. He sounds absurd. Free money is right there!

The Efficient Market Hypothesis is the uncomfortable discovery that, in markets, the old man is almost always right — and understanding why he's right will change how you look at every tip, every headline, and every 'obvious' trade for the rest of your life.

The person behind it: Eugene Fama, a working-class kid from Boston who became the most cited economist of his era. His origin story is perfect: as a student, he was hired to find trading rules that beat the market. He found plenty — they worked wonderfully on past data. Then they met new data, and died. Every time. Fama did what great scientists do with a frustrating result: instead of hiding it, he asked what it was trying to tell him.

(He wasn't the first to hear the message. In 1900, a French mathematician named Louis Bachelier wrote a doctoral thesis showing that prices move as if random — and was ignored for sixty years. This school's Chapter 1 warned you: markets can't be lab-tested, but they can humiliate ideas ahead of their time.)

Fama's answer, published across 1965–1970, is one sentence:

Prices absorb available information almost instantly — so consistently beating the market requires knowing something the market doesn't.

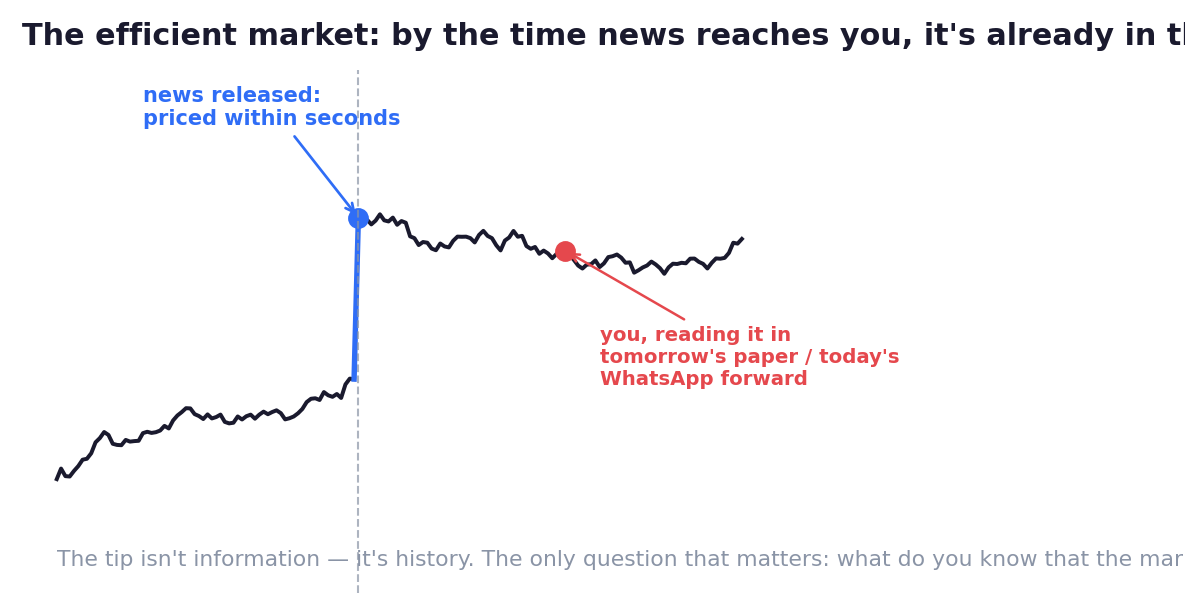

Feel the mechanism, because it's beautiful. What is a price? The live agreement of everyone trading — giant funds, lightning-fast computers, insiders' cousins, and you. The moment new information appears — earnings, a discovery, a war — the fastest money acts within seconds, and its buying or selling pushes the price until the news is 'in'.

So by the time information reaches you — the app notification, the TV panel, the friend's message — the price has already digested it.

The tip isn't information. It's history. Trading on public news is bringing a bicycle to a race against jet engines.

Fama's 1970 paper organised the claim into three strengths, worth knowing in plain words: weak form — past price patterns are already priced (pure chart-reading shouldn't reliably win); semi-strong — all public information is priced (news-trading shouldn't either); strong form — even private information is priced (provably too strong: insiders do profit, which is exactly why insider trading is illegal everywhere).

Now the three twists that make EMH useful rather than depressing:

Twist one — the paradox. The market is efficient because millions of smart, greedy people are trying to beat it. Their collective effort is what prices everything so fast. If everyone accepted EMH and went home, prices would stop reflecting anything — and beating the market would become easy again. Efficiency isn't a wall; it's a tug-of-war that never fully resolves. (Chapter 11 turns this paradox into a full theory.)

Twist two — the gift. In 1976, an American named John Bogle followed EMH to its logical conclusion: if beating the market is nearly impossible after costs, stop paying people to try — own the entire market for almost nothing. The industry mocked the first index fund as 'Bogle's folly'. Today index funds hold a colossal share of the world's wealth and have quietly outperformed most of the professionals who laughed. EMH's greatest output wasn't an argument. It was a product — possibly the most investor-friendly product ever created, available in essentially every country.

Twist three — the honest limits. Markets do crazy things. Bubbles inflate for years. Crashes overshoot. The same asset is priced rationally on Monday and hysterically in a mania. Fama's own Nobel committee made the point with a wink: he shared the 2013 prize with Robert Shiller — the economist who spent his career documenting exactly where efficiency fails. The grown-up conclusion is sharper than either extreme:

*The market prices information brutally fast — and prices emotion badly, repeatedly.* The gap between those two facts is where Chapters 6, 7 and 10 live.

So how do you use this lens? One question, before every single trade, forever:

*"What do I know that the market doesn't?"*

A news item? Priced. A tip? Priced — and you're likely the exit for whoever's selling. A pattern every screener sees? Priced.

But "nothing — I'm buying the whole market cheaply for twenty years" — that's Bogle's answer, and it's excellent. And "my edge isn't information, it's behaviour — I can follow rules and stay calm while others can't" — that's the one edge sixty years of efficiency has never managed to erase. The next chapters explain why.

Key Takeaway

Fama's discovery: prices absorb information almost instantly, because millions competing to beat the market do the pricing — so public news and tips are history by the time you act. Use the one question ('what do I know that the market doesn't?'), index the money with no answer, and remember the honest limit: markets price information fast and emotion badly.

Think About It

Take your most profitable trade of the past year and answer without flinching: did you actually know something the market didn't — or were you paid for a risk you didn't realise you were taking?

Theory Lab — The Other Side of the Trade

For your next five trade ideas, before acting, write one line each: WHO is probably selling this to me (an algorithm? a professional? a panicking holder?) — and why might THEY be wrong?

Rules: if your honest answer is 'no idea', log the idea, skip the trade, and track what it does anyway.

After five ideas, compare your log against one number: what simply buying your local index fund did over the same period.

That comparison — your named edges versus the do-nothing benchmark — is the entire sixty-year EMH debate, running live on your own money, with you as the data.