THE DAMAGE

When

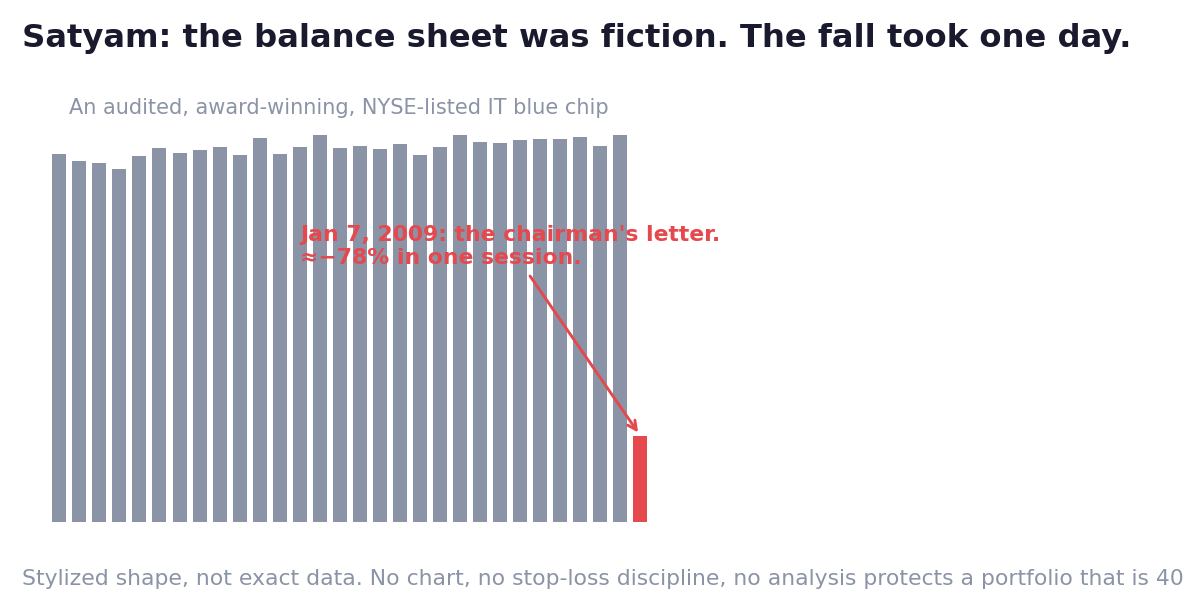

January 7, 2009

Where

Satyam Computer Services — then India's 4th-largest IT company

The fraud

Roughly ₹7,000+ crore of fictitious cash and inflated profits, faked for years

The fall

≈−78% in a single session; included in Sensex/Nifty portfolios and mutual funds across India

What changed

Corporate governance overhaul; auditor accountability; the (renamed) company was rescued via sale to Tech Mahindra

On paper, Satyam was everything an investor is taught to want.

India's fourth-largest IT company. Fifty thousand employees. Global clients. Listed in New York as well as Mumbai. Audited by a Big Four firm. Winner — months earlier — of a Golden Peacock award for corporate governance.

Every box on every checklist: ticked.

On the morning of January 7, 2009, founder-chairman B. Ramalinga Raju sent a letter to the board and the exchanges.

The company's accounts, he confessed, had been faked for years. Of the roughly ₹5,300 crore of cash shown on the books, over ₹5,000 crore did not exist. Profits had been inflated quarter after quarter, and the gap had grown so large it could no longer be hidden.

His letter contained the most famous sentence in Indian corporate history:

"It was like riding a tiger, not knowing how to get off without being eaten."

The stock opened, and simply fell out of the world — down roughly 78% by the close.

There was no warning candle. No chart pattern. No stop-loss that helped — the price didn't pass through levels, it teleported.

And the pain wasn't limited to people who'd 'gambled on one stock.' Satyam sat inside the Sensex and Nifty, inside index funds, inside dozens of mutual fund portfolios, inside crores of retail demat accounts held by people who had done everything right.

Investigations later showed how the tiger had been fed: forged bank statements, fictitious deposits, thousands of fake invoices. The auditors had, for years, accepted confirmations of cash that a single independent letter to the banks would have exposed.

Raju went to jail. The government moved unusually fast, installed a new board, and auctioned the company to Tech Mahindra — saving the employees and clients, though not the shareholders' losses.

Now zoom out, because this file's lesson is bigger than one company.

Technical analysis assumes the chart reflects reality.

Fundamental analysis assumes the numbers reflect reality.

Fraud attacks the layer underneath both. When the raw inputs are fiction, every tool built on them — every ratio, every screener, every fair-value model — is precision-engineering applied to a lie.

You cannot analyse your way out of fraud risk.

You can only size your way out of it.

🦢 Why Nobody Saw It Coming

Satyam wasn't a shady smallcap — it was the establishment itself: index member, Big-Four audited, governance-award-winning, NYSE-listed. The entire system of checks existed precisely so this couldn't happen, and every check said 'safe.' The confession didn't leak out gradually; it arrived complete, in one morning, leaving no exit.

⏳ The Time Machine

If you were there: On January 6th there was nothing to see — no chart pattern, no warning candle. Every protection that worked existed before the letter: a position cap that made Satyam survivable, income not stacked on the same company, and the discipline, once the letter dropped, to refuse 'averaging down on trust' while the facts were still fiction.

If it repeats tomorrow: Cap every stock at a weight whose overnight −78% you can absorb — then fraud becomes a bad day instead of a biography. Watch the few smoke signals fraud emits: promoter pledging spikes, auditor resignations, strange related-party deals. And never let salary, ESOPs and portfolio ride the same name.

🛡️ The Survival Rules

- Cap every single stock. Fraud risk is the final argument for position limits: no single company — however blue the chip — should be big enough that a one-day −78% changes your life. A common discipline: no more than 5–10% of a portfolio in any one stock.

- Audits and awards reduce risk; they do not delete it. Every safety layer around Satyam was real and every one failed. Treat 'fully vetted' as 'less likely', never 'impossible.'

- Never average down on trust alone. When a stock collapses on questions about the numbers themselves, 'it's a great company, it'll recover' assumes facts that may not exist. Facts first, averaging later — usually never.

- Promoter behaviour is data. Heavy promoter pledging, sudden strange acquisitions (Raju's trigger was a blocked attempt to buy his sons' firms), auditor resignations — these are the rare smoke signals fraud gives off. Take them seriously.

- Diversification is the only tool that worked. The investor with 3% in Satyam had a bad day. The employee with salary, ESOPs and savings all in Satyam lost everything at once. Never stack income and investment on the same company.

Key Takeaway

Satyam ticked every checklist — index member, big-four audited, governance awards — and was fiction underneath. You cannot analyse your way out of fraud; you can only position-size your way out. Cap every stock at a size whose overnight death you can absorb.

Think About It

If your largest holding published a Raju letter tomorrow morning — 'the cash does not exist' — what percentage of your net worth walks out with it?

Swan Lab — The Satyam Number

Compute one number: your largest single-stock position as a % of your total portfolio.

That's your Satyam number — the slice of your wealth that one confession letter can vaporise in a session.

Then check two more things for that stock:

Decide your cap — many investors use 5–10% — and write it down as a rule. The cap you set today is the analysis you won't need tomorrow.