THE DAMAGE

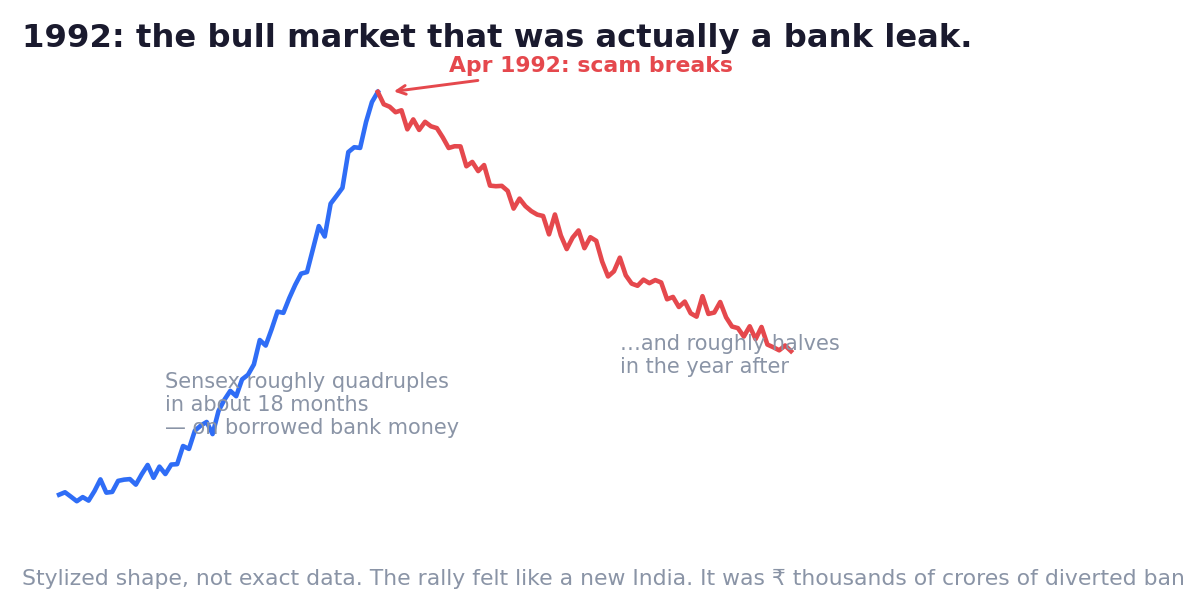

When

Rally through 1991–92; scam exposed April 1992

Where

Bombay Stock Exchange; Indian banking system

The fall

Sensex roughly quadrupled in ~18 months, then roughly halved in the year after exposure

The scam

Estimated around ₹4,000–5,000 crore of bank money diverted into stocks (an enormous sum in 1992)

What changed

SEBI got real statutory powers (1992), NSE was born, screen-based trading and later dematerialisation replaced the old club

In 1991, India had just opened its economy, and one man seemed to embody the new era.

Harshad Mehta. The 'Big Bull'. The man with the sea-facing apartment and the fleet of imported cars, photographed like a film star.

Stocks he touched didn't rise — they levitated. ACC, his favourite, multiplied roughly tenfold. Retail investors followed him blindly; newspapers printed his tips as news.

The market believed it had found a genius.

It had actually found a leak in the banking system.

Here's the scheme, simplified.

Banks in that era constantly lent each other money for a few days at a time, with government bonds as security. These deals moved slowly, on paper, through brokers.

Mehta was one of those brokers — and he found the gap.

Using fake or delayed paperwork (including bogus bank receipts — papers claiming bonds existed where none did), he could sit between two banks and quietly hold the cash in his own account for days or weeks.

Bank A thought its money was safely lent to Bank B.

In reality, it was in the stock market, pumping ACC.

As prices rose, his reputation grew, more money followed him in, prices rose further — the classic loop. The rally looked like a new India's confidence. A big part of it was simply stolen liquidity.

In April 1992, journalist Sucheta Dalal exposed the mechanism.

The money was called back. The pump reversed. The Sensex fell for a year, wiping out lakhs of small investors who had entered at the top because "the Big Bull can't lose."

Mehta faced hundreds of charges and died in jail custody in 2001, cases still pending.

And Indian markets, in the wreckage, got rebuilt: SEBI with teeth, a brand-new electronic exchange (NSE), screen-based trading, and eventually demat accounts — much of the market infrastructure you use today exists because 1992 happened.

But the deepest lesson isn't about 1992's loophole. That one is closed.

It's that the pattern never dies:

A charismatic operator. A story of unstoppable riches. Prices that only rise. A crowd that stops asking where the money comes from.

In the 1990s it was bank receipts.

Today it's a Telegram group, a 'guaranteed' SME stock, a YouTube guru's secret portfolio.

The costume changes. The play doesn't.

🦢 Why Nobody Saw It Coming

Nobody imagined the bull market itself could be the fraud. Investors debated which stocks to buy — not whether the money lifting all of them was real. The system had no independent referee (SEBI had no real powers yet), so the people running the game were the only ones checking the game.

⏳ The Time Machine

If you were there: The tell was visible for months: returns with no explainable fuel, one man's name moving the entire market, and a crowd that had stopped asking questions. The survivor's move wasn't predicting the exposé — it was refusing to hold operator-driven stocks at all, and quietly trimming when the barber, the neighbour and the newspaper all agreed the Big Bull couldn't lose.

If it repeats tomorrow: The 2020s version doesn't wear a suit — it's a Telegram channel, a 'guaranteed' SME stock, a guru's secret portfolio. Run the same audit: find the fuel, refuse rides you can't explain, stay inside regulated channels, and treat 'everyone is making money effortlessly' as the fire alarm it has always been.

🛡️ The Survival Rules

- When returns look magical, find the fuel. Every unnatural rally is powered by something — leverage, diverted money, or a greater fool. If you can't identify the fuel, you're probably it.

- Never confuse a bull market with genius — the operator's, or your own. Rising tides make everyone look brilliant right until the water is called back.

- Operator-driven stocks have exit doors for one. The person who inflated the price sells to you; you cannot sell back to him. Vertical charts on unknown counters are not opportunities — they're queues.

- The pattern repeats in modern costume. Any 'sure thing' whose logic is only 'it keeps going up' — SME pumps, tip groups, guru portfolios — is 1992 with a smartphone.

Key Takeaway

The 1992 rally wasn't investor confidence — it was diverted bank money, and the crowd never asked. When returns look magical, find the fuel. If you can't find it, you are the fuel.

Think About It

The last 'sure thing' you heard about — did you ask where the money pushing it comes from, or only how much of it you could make?

Swan Lab — Find the Fuel

Pick the hottest stock in your watchlist, feed, or tip group right now — the one 'everyone' is buying.

Write one paragraph answering a single question: what is the fuel?

Genuine earnings growth? Index inclusion? Momentum funds? A narrowing float? An operator? A Telegram channel?

If you can name the fuel, you can judge how long it lasts.

If you can't name it after honest effort — write that down too. That's not a gap in your research. That's the answer.