THE DAMAGE

When

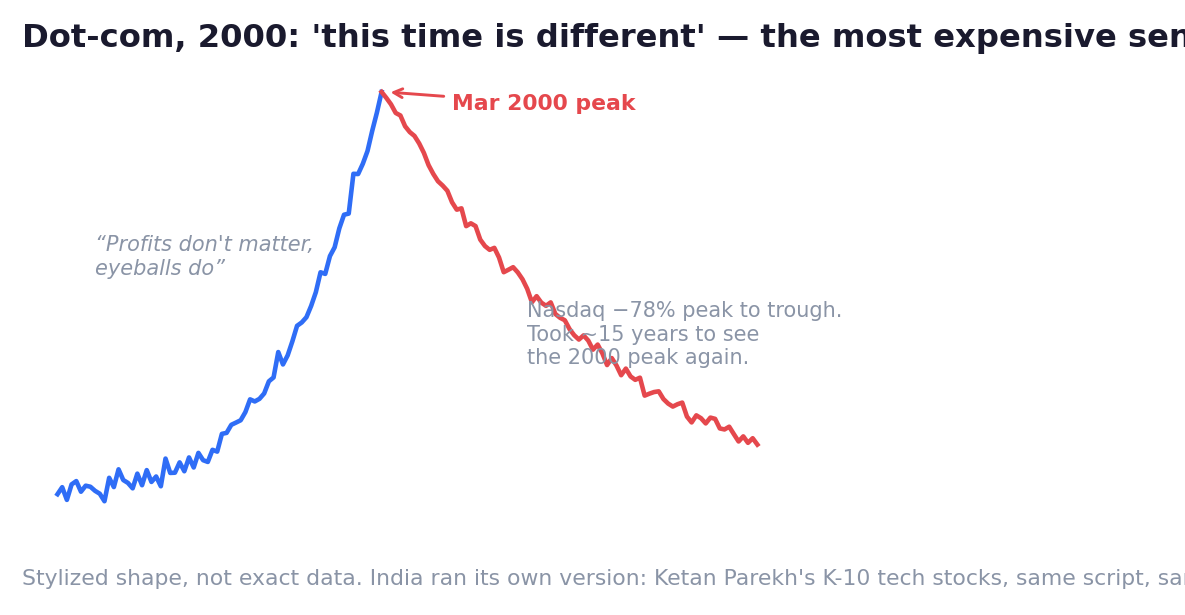

Peak March 2000; the unwind ran into 2002 (India's Ketan Parekh crash: early 2001)

Where

US Nasdaq; Indian ICE (info-comm-entertainment) stocks

The fall

Nasdaq −~78% from peak to trough; many Indian K-10 favourites fell 90%+ and some never returned

Recovery

The Nasdaq needed ~15 years to see its 2000 peak again

What changed

In India: broker-bank nexus exposed, payment crisis at Calcutta exchange, tighter margin & lending rules

By 1999, the internet was clearly going to change the world.

(It did. That's what makes this file so uncomfortable.)

Investors concluded something that felt logical: if the internet changes everything, internet stocks can't be overpriced at any price.

Profits stopped mattering. Companies were valued on 'eyeballs' — how many people visited a website. Firms with no revenue were worth billions. Adding .com to a company's name could double it in a week.

Anyone who mentioned valuation was told they 'didn't get the new economy.'

The four most expensive words in finance had taken over:

*This time is different.*

India ran its own version of the party, with its own Big Bull.

Ketan Parekh, a quiet, well-connected Mumbai broker — a former Harshad Mehta associate — picked ten favourite tech-media stocks, which the market lovingly named the K-10. Using money routed from a cooperative bank and financiers, he ran them up relentlessly. Some multiplied 50 times and more. Retail India piled in behind him, exactly as it had in 1991.

Then, in March 2000, the Nasdaq stopped rising.

No single villain, no single headline. The money simply ran out of greater fools.

The unwind took nearly three years. The Nasdaq lost about 78%. Star companies of the era went to zero. And the index needed fifteen years to see its 2000 peak again — an investor who bought the top in March 2000 waited until 2015 just to break even.

In India, the K-10 collapsed even harder. The 2001 budget-day crash exposed Parekh's funding chain; a payment crisis froze the Calcutta exchange; several K-10 names fell over 90% and some effectively never came back. Parekh was arrested and later barred from the market.

Now, the twist that makes this the most instructive bubble of all:

The internet believers were right.

The technology did change the world. Some of the era's survivors became the most valuable companies in history.

And it didn't matter — because price had left value so far behind that even being right about the future couldn't save you from what you paid for it.

Being right about the story and wrong about the price is still just... wrong.

🦢 Why Nobody Saw It Coming

The mania didn't look like madness from inside — it looked like vision. The doubters had been wrong (and poorer) for five straight years, which felt like proof they'd be wrong forever. Nobody modelled a 15-year recovery, because 'great companies always come back quickly.' Some didn't come back at all.

⏳ The Time Machine

If you were there: You didn't need to short the bubble or call the top — you needed only to notice that price had left value so far behind that even a true story couldn't close the gap. The survivors trimmed as valuations left orbit, capped their tech exposure, and kept owning boring profitable businesses everyone was mocking. The destroyed were 'right about the internet' at 100x sales.

If it repeats tomorrow: Apply it to whatever today's obvious revolution is — AI or anything after it. Two separate questions, always in writing: is the trend real? and what am I paying? Cap any single theme's share of your portfolio, and before buying the story stock, ask the 15-year question: if this takes 15 years to grow into its price, am I still happy?

🛡️ The Survival Rules

- A true story does not justify any price. You can be completely right about a technology — internet, EV, AI — and still lose 80% by overpaying. Separate 'is this real?' from 'what am I paying?'

- 'This time is different' is a sell signal for your scepticism. The words are occasionally true about the world, and almost never true about the arithmetic of valuation.

- Recovery can take longer than your patience, your goals, or your loan. 'It always comes back' hides the questions that matter: when, and does the specific stock you own come back at all? Indexes recover; individual manias often don't.

- When cabs drivers and colleagues who never invested are all in the same trade, the buyers are used up. A rally needs new buyers; a mania eventually runs out of humans.

Key Takeaway

The internet believers were right about the future and still lost 78%, because price had left value behind. Being right about the story and wrong about the price is just wrong — and the wait to break even can be fifteen years.

Think About It

Is there a stock in your portfolio you'd defend with 'this time is different'? What would you tell a friend who used those exact words about a stock you don't own?

Swan Lab — Story vs Price

Pick the stock whose story you love most.

On one line, write the story. On the next, write the price: its P/E (or price-to-sales if there's no E), next to its own 5-year average and its sector's.

Now answer in writing: if the price fell 50% tomorrow, would the story still be true?

If yes — notice what that admits: the story and the price are two different things, and only one of them protects you.

That gap between them is exactly what dot-com investors paid fifteen years to learn.