THE DAMAGE

When

January 2021 (peak: January 28)

Where

GameStop (GME) and other 'meme stocks', US markets

The move

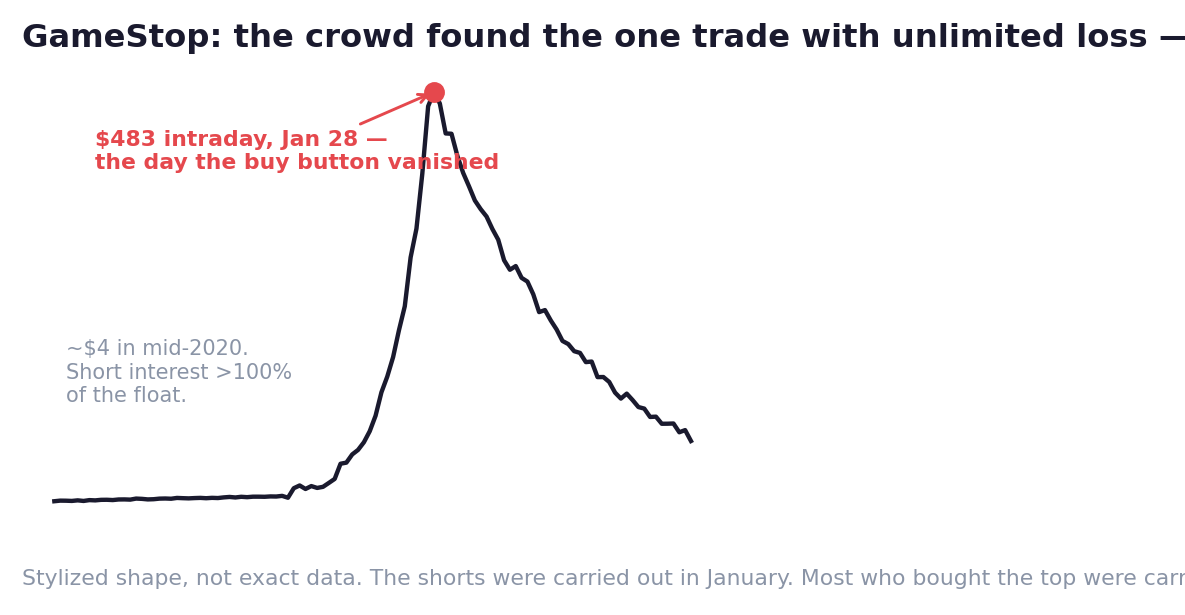

~$4 (mid-2020) → $483 intraday on Jan 28 — a >100x move in a left-for-dead retailer

The casualties

Melvin Capital lost ~53% in a month and needed a bailout; late retail buyers rode the stock down ~90% from the peak

What changed

Congressional hearings; scrutiny of payment-for-order-flow, brokerage capital rules and short-interest reporting

GameStop was a chain of video game stores in shopping malls, in an age of downloads and dying malls. Wall Street's verdict was unanimous: a corpse.

Hedge funds expressed that verdict the aggressive way — short selling: borrow shares, sell them, buy them back cheaper later. So many funds piled on that reported short interest exceeded 100% of the available shares. More shares had been sold short than existed to buy back.

On a Reddit forum called WallStreetBets, a few users did the arithmetic that the professionals apparently hadn't:

If we buy and simply refuse to sell... the shorts eventually have to buy from us. At any price we name.

To understand the trap, understand the asymmetry — the single most important line in this file:

When you buy a stock, your maximum loss is 100%. When you short a stock, your maximum loss is unlimited — because there is no ceiling on how high a price can go, and you must buy back.

A falling price politely asks a shareholder if he'd like to sell.

A rising price forces a short seller to buy.

Through January 2021, the crowd bought. The price rose. Rising prices forced shorts to buy back, pushing prices higher, forcing more shorts to buy — the same doom loop as 1987's portfolio insurance (Chapter 03), running in reverse, with rocket emojis.

$20. $40. $76. $148. $347. On January 28: $483 — from $4 seven months earlier. Melvin Capital, the most prominent short, lost over half its fund in a month and needed a multi-billion-dollar rescue.

Then came the twist nobody had priced: the buy button disappeared.

On January 28, Robinhood — the brokerage where much of the crowd traded — blocked buying of GameStop (selling remained allowed). The real reason was plumbing: the clearing system demanded billions in collateral the broker didn't have. The effect was the same either way — at the peak of the battle, one side's weapon was confiscated. The price collapsed within minutes.

And the ending had no winners' podium. The shorts were carried out in January. The stock then fell roughly 90% from its peak — carrying out everyone who had bought near the top 'because it was going to $1,000.' The early Redditors who sold into the squeeze won; the crowd that joined the crowd financed their exit.

A mania is a room that pays whoever leaves early and bills whoever arrives late.

🦢 Why Nobody Saw It Coming

The professionals' models had no variable for 'a coordinated internet crowd with stimulus cheques and nothing to lose.' Short interest above 100% of float was public data — the loaded gun was lying in the open — but 'retail can't move a stock against us' was an assumption so deep nobody checked it. And no one, on either side, had modelled a broker turning off the buy button.

⏳ The Time Machine

If you were there: Every seat at that table had a different correct move. The shorts' was to never be naked short 100%+ of a float — and once squeezed, to cover early rather than argue. The early longs' was to sell into the vertical, not at it. The crowd's was to recognise that joining a mania at $300 wasn't the trade — it was the exit liquidity. And everyone learned the buy button belongs to the broker.

If it repeats tomorrow: Never carry unlimited-loss positions into crowded territory — express bearish views with defined-risk instruments. Never buy a vertical chart because it's vertical. Check how crowded your 'obvious' trade is before entering, and factor in platform risk: in the next squeeze, assume some broker, somewhere, turns something off at the worst moment.

🛡️ The Survival Rules

- Never sell naked unlimited risk. Shorting stocks (or selling uncovered options) means your worst case has no floor under it — one crowded, irrational month can erase a decade. If you must bet against something, use instruments with defined risk, like buying puts.

- Never short a mania, never marry one. 'It's obviously overvalued' is true and useless — the market can stay irrational longer than you can stay solvent. And buying a vertical chart because it's vertical makes you the exit liquidity.

- Crowded trades reverse violently. Whether it's everyone short (GameStop) or everyone long (dot-com), when a trade becomes a crowd, the exit becomes a door for one. Check how crowded your 'obvious' trade is.

- Platform risk is real risk. Your broker, in extreme conditions, can restrict your ability to act — for regulatory, capital or plumbing reasons. It has happened and will happen again. Factor it into position sizes; consider not keeping everything with one broker.

- In any mania, know which character you are. Early conviction, or late imitation? If your only reason to buy is that it's already up 500%, you're not in the trade — you're in the story's final chapter.

Key Takeaway

GameStop proved shorting has unlimited loss, crowds can out-stubborn professionals, and your broker can switch off the buy button at the worst moment. Both sides lost; only those with defined risk and an early exit won. Never carry a position whose worst case has no floor.

Think About It

Which position in your book right now has a worst case you have never actually calculated — and is 'it won't happen' the only thing standing between you and it?

Swan Lab — The Unlimited-Loss Hunt

Go through every open position and write its theoretical worst case in rupees:

Flag everything unlimited or account-threatening.

For each flag, decide today: close it, hedge it into defined risk, or consciously accept it in writing. The one rule: no position stays unexamined.