THE DAMAGE

When

Black Thursday, Oct 24, 1929; Black Monday & Tuesday, Oct 28–29; the slide ran to July 1932

Where

US markets; the depression that followed went global

The fall

Dow ~381 (Sep 1929) → ~41 (Jul 1932): −89%

Recovery

The 1929 peak was seen again only in November 1954 — 25 years later

What changed

The modern rulebook was born: the SEC, margin regulation, deposit insurance — investor protection as we know it

The 1920s in America felt like the future arriving all at once.

Cars. Radio. Electricity in every home. An economy roaring, a war won, a new era declared.

And for the first time in history, ordinary people poured into the stock market — clerks, teachers, drivers — because the market only went up, and everyone knew someone getting rich.

But the real engine of the boom wasn't optimism.

It was margin.

Brokers would happily lend you 90% of a stock's price. Put down ₹10, control ₹100. If the stock rose 10%, you doubled your money.

Millions did exactly this. Nobody dwelt on the mirror image: if the stock fell 10%, you were wiped out completely — and the broker would sell your shares to recover his loan, whether you agreed or not.

An entire market was now a pyramid of borrowed money, balanced on prices never falling.

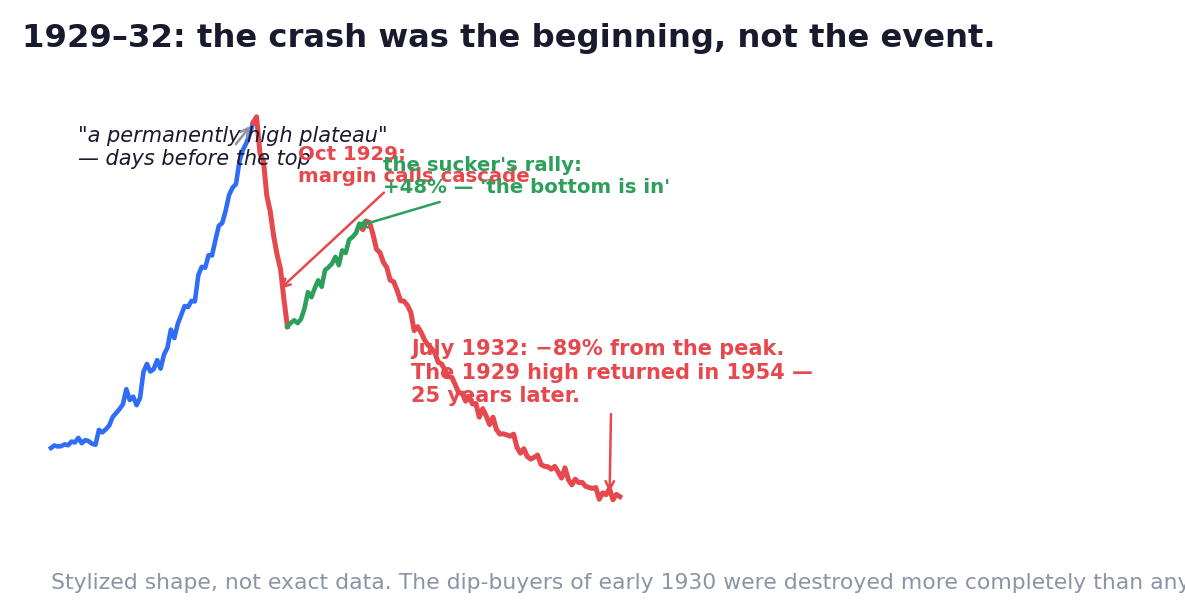

At the very top of the mania, Irving Fisher — the most celebrated economist in America — gave the moment its immortal words:

"Stock prices have reached what looks like a permanently high plateau."

That was mid-October, 1929.

On Thursday, October 24, the plateau cracked. Panic selling hit; a pool of powerful bankers stepped in, publicly bought shares, and steadied the day — the way it had always worked before.

It worked for two days.

On Monday the 28th, the Dow fell nearly 13%. On Tuesday the 29th — Black Tuesday — another 12%, on volume so enormous the ticker ran hours behind, so sellers couldn't even learn what price they were being executed at.

Here's the machine that did it — learn it once, because you'll meet it again in 1987, 2008 and 2024:

A falling price triggers margin calls. Wiped-out borrowers' shares are force-sold by brokers. Forced selling pushes prices lower. Lower prices trigger the next layer of margin calls.

The original doom loop. No computers required.

Now the part of the story almost nobody knows — and the most practically useful part of this whole chapter.

The October crash was not the disaster. It was the trailer.

By spring 1930, the market had rallied back nearly half of its losses. Newspapers declared the storm over. The 'smart money' that had missed the top bought this dip with everything.

That bounce is remembered today as the sucker's rally.

From there, the market slid — slowly, grindingly, for two more years — another 80% down. The dip-buyers of 1930 were destroyed more completely than anyone caught in October.

Around them, the economy itself collapsed. Thousands of banks failed — and with no deposit insurance yet, when a bank died, the savings inside it died too. Unemployment reached roughly a quarter of the workforce. People lost their jobs, their portfolios and their bank accounts — the same people, all three, at the same time.

The bottom came in July 1932: the Dow at 41, down 89% from a peak that had been declared permanent.

An investor who bought that peak and simply held waited until 1954 — twenty-five years — to see it again. (Counting dividends and the era's falling prices, the true wait was nearer a decade — still longer than most careers, loans and retirements can afford.)

Out of the wreckage, the modern market was invented: a securities regulator with teeth, strict margin limits, insured bank deposits.

Every protection you take for granted today is scar tissue from 1929.

🦢 Why Nobody Saw It Coming

The smartest people alive had data proving a new era — and the data was even partly true. What nobody could see was the pyramid of 10:1 loans underneath prices, because leverage hides until it's triggered. And nobody planned for a generation-long recovery, because in their data, the market had always come back quickly. The turkey's chart, at national scale.

⏳ The Time Machine

If you were there: The single decision that separated survivors was refusing 10:1 margin in September 1929. Even simply holding through the whole horror worked eventually — but only for those with no leverage, an income, and savings outside the market. The two fatal trades: margin at the top, and buying the 1930 bounce with everything, convinced the bottom was in.

If it repeats tomorrow: Treat leverage limits as law. Assume the next crash may be an L, not a V — so money with deadlines stays out of the market entirely. Keep your income and emergency fund independent of your portfolio. When a crash rallies 40–50%, remember 1930 before announcing the bottom — re-enter in instalments. And keep the small, boring, regular buying going: the accumulator of the 1930s beat the lump-sum genius of 1929 by decades.

🛡️ The Survival Rules

- Margin is the crash accelerant. At 10:1, a −10% move erases you while the index still has −79% left to fall. Every rupee of leverage shortens the fall you can survive — decide yours using 1929, not last quarter.

- Plan for the L, not just the V. 2020 recovered in months; 1929 took a generation. A plan that silently requires a fast recovery isn't a plan — it's a bet on which century you're in.

- Beware the correlated catastrophe. 1929 took jobs, portfolios and bank savings from the same families at once. Real safety is income + insured cash + investments that don't all ride the same economy the same way.

- Relief rallies lie. A +48% bounce preceded another −80%. A rally is not evidence of a bottom; re-enter in planned instalments, never in one grateful lump.

- The boring accumulator wins the long game. Those who kept buying small, regular amounts through the 1930s were made whole years — decades — before the lump-sum buyer of the top.

Key Takeaway

1929 wrote the template: leverage builds the top, margin calls build the bottom, and recovery is promised on nobody's timeline — 25 years for the top buyer. Survive on zero margin, outside income and insured cash, and treat every relief rally as a suspect, not a saviour.

Think About It

Does your financial plan survive a recovery that takes 25 years — or does it silently assume the market must come back within two or three?

Swan Lab — The Plateau Test

Write down the sentence you most believe about today's market — "India's decade", "AI changes everything", whatever it is.

Directly underneath it, copy this: "Stock prices have reached a permanently high plateau." — October 1929.

Now run three checks:

No forced-selling level, nothing breaks, instalments planned — you've already graduated from 1929. Anything else is this chapter's homework.